The Wall Street Journal just published a piece on the same Compass ultra-luxury report I shared last week, and it's worth reading for the specific market stories behind the numbers.

A few things that stood out:

Los Angeles's turnaround was dramatic. The city entered 2025 still dealing with the mansion tax fallout, which had frozen the high end for nearly two years. Sellers finally adjusted expectations in 2025, and transactions jumped 54%. The wildfires added complexity, with some displaced buyers using insurance proceeds to relocate within LA or move to markets like Santa Barbara entirely.

San Francisco's rebound mirrors tech momentum. Sales over $10 million jumped 50% in 2025 after years of sluggish activity. The AI boom created concentrated wealth competing for limited inventory. One agent quoted in the piece said that in 2023 and 2024, "you couldn't give stuff away." By late 2025, everything was moving fast. Silicon Valley overall saw 36% growth with only 1,000 homes for sale across the entire market.

Emerging markets are no longer anomalies. Phoenix, San Diego, and Dallas all posted record-breaking $10M+ sales. A $50 million Del Mar property set a San Diego County record. A $225 million Naples estate became the priciest US sale of the year. These aren't traditional ultra-luxury hubs, but they're attracting serious capital from buyers seeking lower taxes, better inventory, or geographic diversification.

The "safe-deposit box" mentality persists. Despite geopolitical uncertainty and questions about an AI bubble, ultra-high-net-worth buyers continue viewing real estate as a stable store of value. It's a tangible asset that provides utility while holding capital, not just paper appreciation.

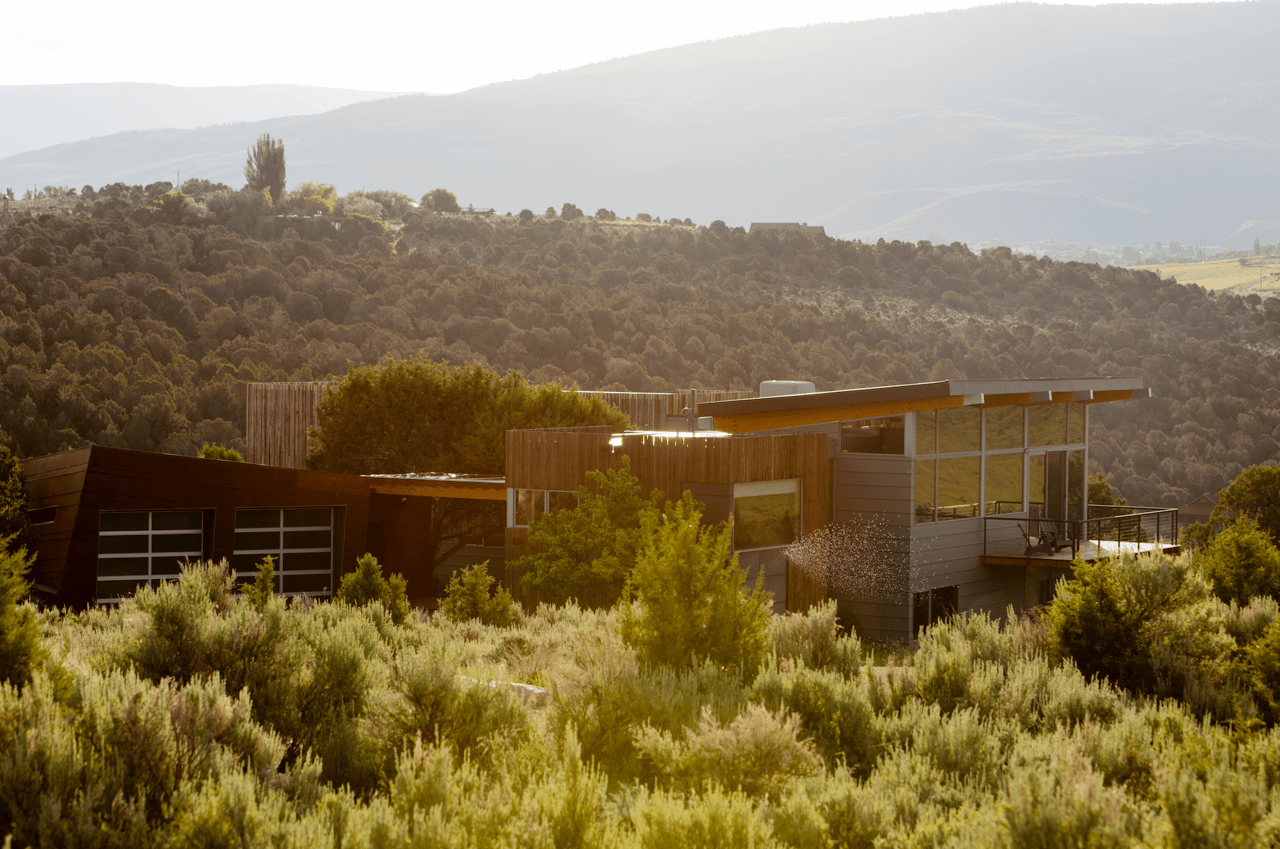

For Aspen, the dynamics are similar. Buyers here prioritize properties that deliver on location, quality, and immediate availability. Aspirational pricing without substance doesn't move. The properties that succeed are the ones that justify their value through execution and get buyers into homes without long timelines.